Pason Systems

As always, this should not be considered investment advice. Please do your own research and verification.

This post is on Pason Systems, $PSI.TO, which I touched upon briefly in my post “Recap of Recent Portfolio Activity”.

Idea Generation: Pason Systems came onto my radar when I ran a screen on Canadian companies with 15-25x EV/EBIT multiples that had delivered high EPS growth rates from 2013-2022. A brief but good write up on the company on VIC that was done just before the pandemic helped as an intro to the company, and I was intrigued by the shareholder base. I ended up making a small purchase in early April at $12.15 after the stock experienced a 25-30% drop with the intention of doing some more work on the name to see if it would be something worthwhile of a larger position size - this post is the byproduct of having done a little more work.

Brief Overview & Business Quality: Pason is a technology-oriented oil services company that provides data management systems for drilling rigs around the world, though most of its revenues are in North America. The chart on the left hand side below does a good job of illustrating how the overall direction of the companies revenues has historically been tied to changes in North American rig counts.

That kind of cyclical profile may be enough to turn a lot of investors off, but the graph on the right hand side above could peak some interest: despite declining overall revenues following the oil collapse in late 2014 Pason was able to maintain and then growth its revenue per industry day in the years that followed. The ability to maintain pricing in this environment is likely due to the market structure of the industry Pason operates in (Pason has leading market share within an oligopoly) and fact that their product is an operational necessity, as drillers are required by regulation to track and report certain variables, and PSI's products help them do that. The company’s large existing installed-base of sensor packages on systems makes the business very high margin and quite capital-light on a go-forward basis.

In addition to strong profitability, $PSI.TO has historically been run with a clean balance sheet. This allowed the company to avoid cutting its dividend in the mid-2010’s downturn, which it continued to fund with internally generated cash flow and avoid raising any additional debt or equity - this ability to operate without a reliance on accessing capital markets is something which has differentiated Pason from many of its Energy Service peers over the past decade.

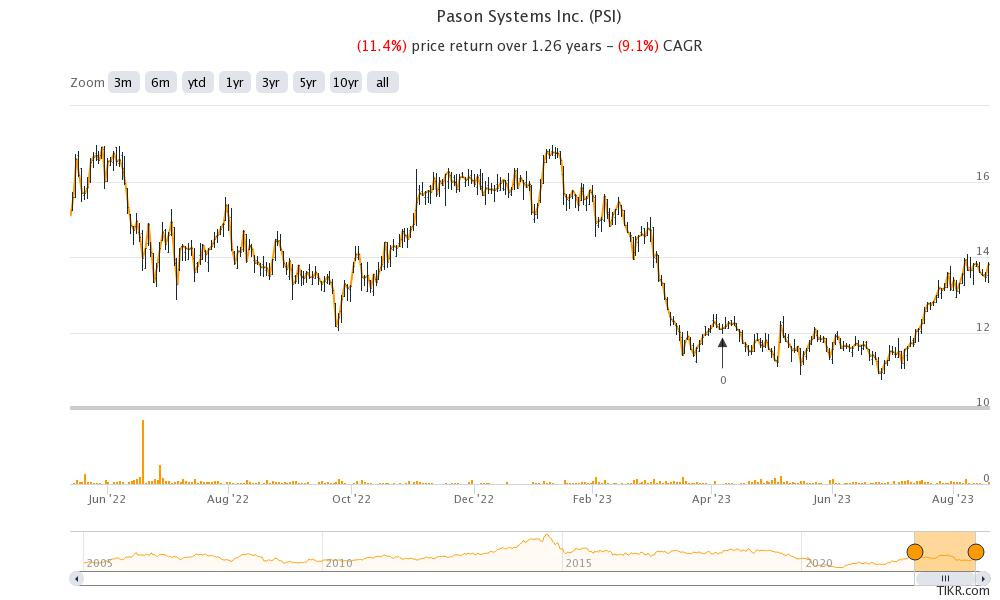

What’s New: Following the 2014 commodity bust Pason’s stock mostly traded between $15 and $22, though leading up to the pandemic it continued to decline, trading down to $12-$13.

With the stock trading around $13.50 today, shy of where it was for most of 2015-2019, it seems fair to ask what has changed in comparison to the pre-pandemic period and if the decline in share price is justified. I actually find there to be quite a few positives when doing this exercise:

Improved Pricing: As noted earlier, the company has managed to improve revenue per industry day via increased pricing and upselling of its services, leading to Pason’s current overall profits exceeding pre-pandemic levels despite lower rig counts.

Industry back drop: The tightness of supply in the oil market is something which has come into focus over the past couple years after experiencing both the up and down portions of a long CAPEX cycle within the industry. Pason’s MDA:

With production, crude oil and product inventories and the inventory of drilled but uncompleted wells (DUCs) all below pre-pandemic levels, any efforts to increase supply will require additional drilling activity.

Paired with a look at where the land rig count in North America stands vs the past several years, there is a case to be made that Pason’s business may stand to benefit from a cyclical upswing.

Change in Capital Allocation: While Pason didn’t cut it’s dividend in the mid 2010’s, it did reduce it during the pandemic and management has since stated that it intends to continue with the lower payout ratio which enables greater flexibility in capital allocation. Despite the lower payout ratio the stock’s dividend yield is comparable to pre-pandemic levels.

Sharecount: The company’s shares outstanding are down about 6% from its peak. By no means a huge reduction, but better than nothing.

Interest Income: The rise in interest rates has led to the company’s cash balance generating a material amount of interest income for the company (approx. 10M per year).

Investments: Since 2019 Pason has made a considerable amount of investment into its stake in Energy Transfer Base (ETB) and Intelligent Wellhead Systems (IWS); Pason has directed 50M into IWS and I estimate the majority ownership stake in ETB, along with subsequent R&D investment in the business and costs incurred as it has been loss-making, add up to another 50M. The combined 100M is not a small sum for a roughly 1B market cap company and investors may prefer to have seen that capital allocated differently. The question mark about what ROIC will be generated on these investments and how much more cash flow will be directed into such initiatives, paired with a management team that doesn’t own a ton of company stock seems to me like a plausible case for why Pason is trading where it is today vs pre-pandemic.

However, I think there’s been some recent data points that suggest these investments may actually end up being fairly profitable:

ETB, the company’s solar and energy storage division, is growing quite rapidly at the moment and approaching break-even profitability: segment revenues are now around 2.5M per quarter vs sub 1M when ETB was acquired in 2019 and over the past few quarters growth in expenses has been levelling off to the point where revenues are now over 90% of operating expense, after being sub 70%,

Meanwhile, Pason’s non-controlling stake in IWS looks to be profitable as suggested by:

positive share of after-tax income recorded on Equity Investments in 2022’s Annual Report

Consecutive quarters of equity income (bucking a string of losses) in Q1 and Q2 2023

Recent decision for PSI to finance IWS via preferred shares instead of equity.

Should these two investments prove to be successful, they could produce an amount of cash flow which is material to Pason in the future.

Valuation/Other: While revenues can certainly fluctuate substantially year-over-year I think there’s a good chance Pason will see greater free cash flow generation in the years to come than they have been: a cyclical upswing in drilling activity, growth and improved margins in its international business (Int’l represents less than 20% of Sales and gross margins in Int’l are 15-20% below North America), continued adoption of its full suite of services to drive growth in Revenue per Industry Day, and cash flow generation from investments in IWS and ETB all present possible growth drivers for the company and do not require much in the way of capital.

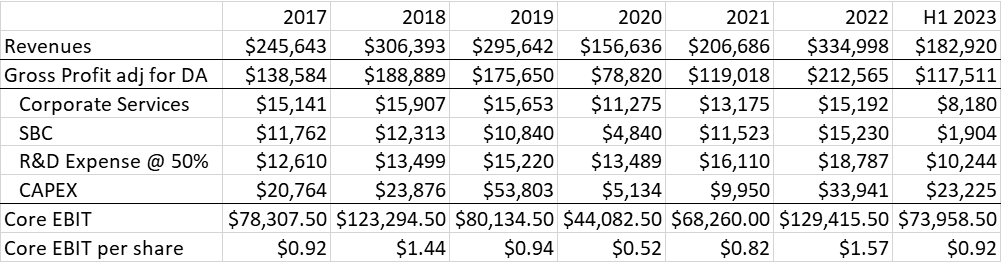

In the meantime, Pason is generating a lot of cash flow; here’s a quick sketch of what EBIT from the core business looks like prior to adding back interest income from its cash balance (call it another 13 cents per share in EBIT).

That’s certainly not an exhaustive table - for example, the company had a string of FX losses throughout 2017-2020 and H2 2023 that aren’t accounted in the above table - and some may disagree with my treatment of categorizing 50% of R&D as investment instead of maintenance, though I would counter that by stating I’m also treating all CAPEX here as maintenance CAPEX and none as growth.

Regardless of how you view the historical numbers, PSI has been generating quite a bit of cash flow while making investments through the income statement. My belief is that FCF of $1.50 per share is well within reach for the company and does not constitute “peak cyclical earnings”. With no debt and a handful of visible drivers for future increased cash flows, the stock seems attractively priced to me trading in the low teens, so I decided to add to my position following the release of Q2 earnings just under $13.50 bringing my weighting in the name up to 10%.